plan to invest for the future.

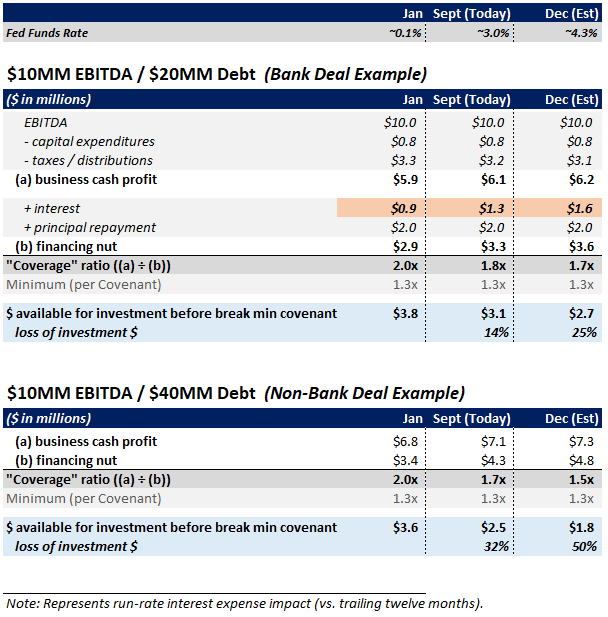

One result of rising rates will be less money available for borrowers to invest in their businesses. A way you could measure this is by looking at the impact on a company's ability to cover its "financing nut", or the yearly cost of its borrowed money. The bigger the nut, the more significant the reduction to "money available to invest for the future" (for some, up to 50%).

Borrowers make promises to their lenders - one being they'll be able to repay their debt, which is regularly verified by measuring the company's vitals and ensuring they are within a healthy range. A standard vital is the "coverage test" - comparing (a) my business's cash profit vs. (b) how much I paid my lender (principal + interest) over the last year, or my financing nut.

As rates and interest rise, the financing nut grows and the cushion between current and acceptable coverage decreases - dollars that could be reinvested in the business. Absent higher sales to offset the impact, companies forgo planned investments to compensate - e.g., new hires, systems upgrades, additional equipment, etc. The below shows the reduction in money available to invest due to rising rates for two companies with $10MM of EBITDA - one with $20MM of debt (bank deal) and one with $40MM of debt (non-bank / direct lender deal; bigger financing nut = bigger reduction).

The Uncommon Borrower plans to invest for the future - they 1) forecast the next 12-24 months of credit vitals, 2) identify cushion and points of tightness, and 3) thoughtfully carve out budgeted investments ahead of time.